The banquet of consequences is not fully served yet.

“The process by which financial markets, financial institutions, and financial elites gain greater influence over economic policy and economic outcomes is not a side effect of capitalism. It is the replacement of capitalism.”

— Gerald Epstein, Financialization and the World Economy, 2005

I. The Bait and Switch

Most Americans understand capitalism the way they understand electricity: they use it constantly without thinking about how it works, and they notice it only when it fails. The standard model is simple enough. People work. They produce things. They trade. Prices signal where effort should go. Capital flows toward productive use. The system isn’t fair — nothing is — but it creates real wealth because it is grounded in real activity.

What has been operating in the United States for the last fifty years is not that system. It is something built on top of that system, extracting from it, progressively hollowing it out. The name for it is financialization: the process by which the financial sector stops being the servant of the productive economy and becomes its master — allocating fake money toward existing assets rather than real capital toward productive use, extracting returns from position rather than from creation.

The bait was capitalism. The switch happened so gradually that most people never noticed the moment it occurred. By the time the consequences became visible — in the form of a productive economy that doesn’t produce much anymore, wages that don’t buy what they once did, and a financial sector that claims an ever-larger share of national income while contributing an ever-smaller share of national output — the architecture was already load-bearing.

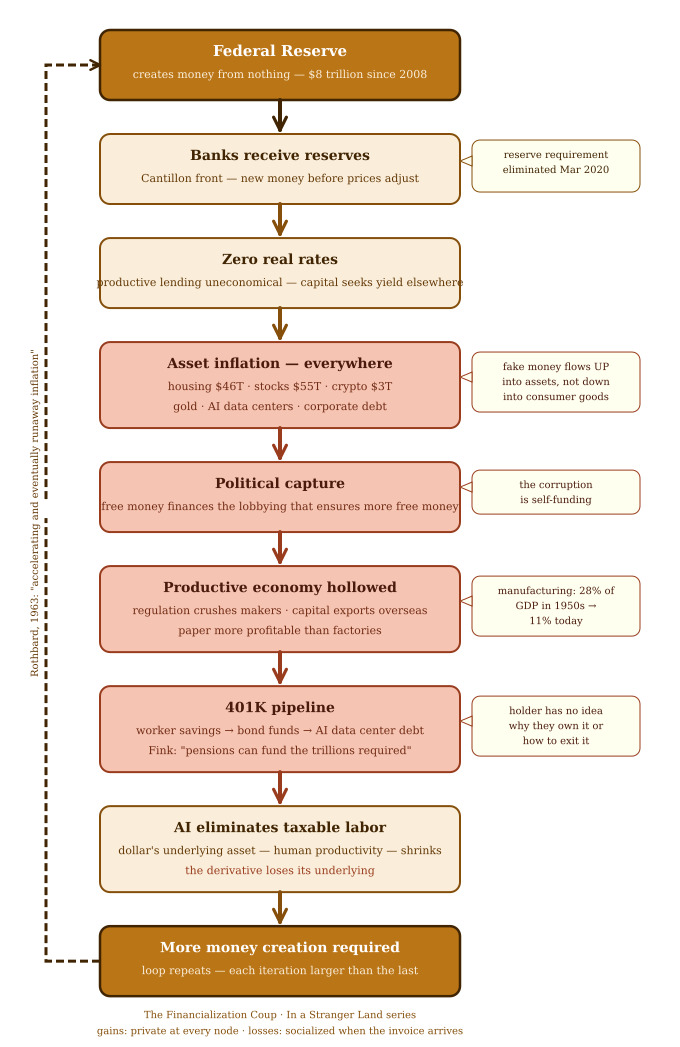

II. The Cantillon Front

The mechanism has a name, and it has been understood since the 18th century. Richard Cantillon, an Irish-French economist writing in the 1730s, observed that newly created money doesn’t distribute itself evenly across an economy. It enters at specific points — through specific institutions and individuals — and moves outward from there. Those closest to the point of entry receive the new money before prices have adjusted to reflect its existence. They spend it at old prices. By the time the money reaches those furthest from the point of entry — wage earners buying groceries, workers whose salaries are renegotiated annually — prices have already risen to reflect the additional money in the system. The purchasing power was extracted during the journey.

It is tempting to read this as a one-sided story: those at the front of the line get a free ride at old prices, while those at the back simply pay a proportionally higher price reflecting the larger money supply. There is no free ride. Someone always pays — and the mechanism by which they pay is more punishing than a simple average price increase. The wage earner at the end of the chain does not merely receive a price that reflects the new money’s average effect on the price level. He pays a price that has compounded through every transaction the money passed through before reaching him — because every producer along that chain, having paid inflated prices for the inputs that Round 1 spenders had already bid up, must in turn raise his own price to recover that cost. This is the transmission cost of inflation: not a single markup applied once at the cash register, but a markup added and compounded at every link in the supply chain between the point where the money entered and the point where the wage earner finally spends it. The end of the line is not simply receiving devalued purchasing power. It is subsidizing the markup of everyone who stood closer to the spigot.

This is the Cantillon Effect. It is not a conspiracy. It is not a policy failure. It is the documented, predictable, mechanical consequence of money creation in a system where money enters through specific institutions rather than distributing simultaneously to everyone.

The Federal Reserve creates money by purchasing assets and crediting banks with reserves that didn’t previously exist. The banks are at the front of the line. Since 2008, the Fed has created approximately $8 trillion this way. Under the old 10% reserve requirement, each Fed dollar supported $10 in bank lending — $80 trillion in money that didn’t exist before. On March 15, 2020, the Fed eliminated reserve requirements entirely. Not reduced. Eliminated. The theoretical leverage became infinite.

The $80 trillion had to go somewhere. It did not go into wages. It did not go into new factories. It went into assets — because assets are what the institutions at the front of the Cantillon line actually buy. US residential real estate swelled to $46 trillion in total value. The stock market reached $55 trillion in capitalization — not because American companies became more productive, but because the money was there and it needed a return. Cryptocurrency absorbed another $2-3 trillion at peak, pure belief derivative with no coercive enforcement behind it. Gold and silver, the historical refuges from monetary debasement, were bid up multiples beyond their 2008 prices. The AI data center buildout of 2023-2026, presented as a technological revolution, is in structural terms a $1 trillion debt-financed construction boom built on balance sheets themselves inflated by fifteen years of cheap money.

The inflation ordinary Americans experience at the grocery store is real but modest by comparison. Retail prices are disciplined by global competition and supply chain efficiency in ways that asset prices are not. The fake money flows upward into assets — because assets are what those at the front of the line buy. The Cantillon Effect is not a market outcome. It is a policy outcome. And it runs on schedule.

III. The Feedback Loop

The standard critique of financial inequality stops here: the rich get richer because they own assets and assets inflate. This is true but incomplete. It describes a static condition. What actually exists is a dynamic system — a feedback loop with three phases that reinforce each other without external intervention required.

Phase One: Capture. The Cantillon front-runners receive cheap money, deploy it into appreciating assets, and accumulate wealth disproportionate to any productive contribution. This is the standard Austrian critique, documented in detail since Mises and Hayek identified the mechanism in the 1920s.

Phase Two: Entrenchment. The accumulated wealth gets deployed into the political system — lobbying, regulatory capture, revolving door employment, campaign finance — specifically to preserve and extend the conditions that produced it. The banks that were too big to fail in 2008 are larger now. They used the bailout money to purchase the political protection against the structural reforms that would have constrained them. The mechanism was not subtle. It was documented in Congressional testimony, in lobbying disclosures, in the careers of Treasury officials before and after their government service. It happened in plain sight because there was no political force with both the incentive and the capacity to stop it.

Phase Three: Dependency. The system becomes self-reinforcing in a specific and underappreciated way: the financial sector now requires continued monetary expansion to service the debt structures built on the assumption of it. Every serious tightening cycle since 2008 has been reversed before completion — 2018, 2019, 2022 — because the asset price structures that depend on cheap money begin to crack under genuine tightening, and the same institutions that caused the problem have enough political influence to ensure the cure is administered in insufficient doses. The system cannot tolerate the medicine because the disease has become structural.

The key insight is this: the free money doesn’t just enrich the front-runners. It finances the political apparatus that ensures the front-running continues. The corruption is self-funding. The Federal Reserve’s money creation directly finances the lobbying operation that ensures the Federal Reserve continues creating money. The loop closes.

IV. The Workers Pay the Bill

While the financial sector extracted returns for the privileged, something was happening to the economy underneath it.

Manufacturing’s share of US GDP peaked at approximately 28% in the late 1950s. It is now approximately 11%. This is described in mainstream economic commentary as the natural progression of a maturing economy — services replacing manufacturing as the dominant sector, as happened in every advanced economy. The description is accurate. The explanation is incomplete.

Capital went overseas not because American workers became uncompetitive in any natural sense. It went overseas because the regulatory and legal infrastructure made domestic production structurally uneconomical — while financial engineering remained extraordinarily profitable and faced none of the same friction costs. A manufacturer who wants to build a factory in the American midwest faces years of environmental review, union negotiation, zoning variance, OSHA compliance, and tax structure complexity before producing a single unit. A financial instrument faces no NEPA review. A derivative clears in milliseconds. The same capital that would have taken seven years to deploy in a manufacturing plant can be deployed in financial markets this afternoon.

This was not an accident of history. It was a policy choice, made incrementally over decades, that made paper more profitable than factories. The regulatory burden that crushes small manufacturers can be absorbed by large incumbents as a moat against competition. Every additional compliance cost that a major bank or major corporation can amortize across large revenue bases, but a new entrant cannot, is a barrier to productive competition built with government materials. The regulatory state and the financial oligarchy are not in tension. They are partners.

The China comparison is analytically precise and politically inconvenient: a manufacturer who wants to build in certain Chinese industrial zones breaks ground in months. The Pax Silica alliance — the US-led diplomatic framework for securing AI supply chains, formally launched in December 2025 — is partly an acknowledgment that American productive capacity has been regulated and financialized into nonexistence while China kept building things. You cannot alliance-build your way around a refinery you chose not to build. You cannot sign a declaration that replaces the industrial policy decisions that weren’t made between 1980 and 2020.

But being first in line for free money was not enough. They actually paid money to the banks to hold the free money! Interest on Excess Reserves, authorized by Congress in 2006 but deliberately scheduled five years out to delay its budgetary cost — then accelerated to October 2008, weeks after Lehman collapsed, buried in the same emergency legislation that authorized TARP. The Fed created trillions in new reserves to rescue the banking system, then began paying the same banks not to lend that money out. The monetary base nearly doubled within a year, but the broader money supply barely moved — because banks found it more profitable to sit on freshly created reserves, collecting a riskless government check, than to lend into an uncertain economy. The bailout didn’t need to show up as inflation at the grocery store. It only needed to show up on a bank’s balance sheet as an asset earning interest from the same institution that had just created the asset out of nothing. The banks were paid, quietly and indefinitely, to hold the very money that was supposed to prove the rescue worked.

Mom-and-pop stores did not get an emergency lending facility after the 2008 crisis. They did not get a guaranteed, risk-free, interest-bearing account at the Federal Reserve. They got the recession the banks had caused, in full, with nothing to cushion the fall. The asymmetry was not incidental to the bailout — it was the bailout’s actual design. Newly created money flowed first to the institutions closest to the Fed, who were then paid to keep it rather than lend it back into the businesses and households who needed it to survive the downturn those same institutions had created. The wealthy got insulated from their own failure. Everyone else got the consequences of it. One institution’s mistake, fully covered. Everyone else’s mortgage, fully exposed.

What’s called “capitalism” in American political discourse is increasingly the financialized, regulatory-captured variant — not free markets but a specific kind of mercantilist cartelism that benefits incumbents and punishes new productive entrants. The label survives. The substance it described is largely gone.

V. August 15, 1971 – A Day which will Live in Infamy

The previous section described capital fleeing the productive economy for financial engineering — but the trigger for that flight has a precise date. On August 15, 1971, President Nixon announced that the United States would no longer convert dollars to gold at the request of foreign governments. The arrangement had constrained American deficit spending and monetary expansion since Bretton Woods in 1944 — any government printing too many dollars risked a run on its gold reserves. Nixon’s announcement, delivered on a Sunday evening television broadcast and framed as temporary, permanently severed that constraint. It has never been restored.

The pattern is so consistent across so many unrelated domains that an entire site — wtfhappenedin1971.com — exists solely to catalog it. Wages and productivity. Inequality. Savings rates. Family formation. Incarceration. Energy use. Even what kinds of meat were consumed. Dozens of charts spanning economics, sociology, and diet, drawn from primary government sources, every one of them bending at the same date: August 15, 1971, the day Nixon closed the gold window. No single chart proves causation. Dozens of unrelated charts inflecting at the identical moment is not coincidence — it is the signature of a constraint being removed from the entire system at once. The site’s epigraph, from Hayek in 1984, states the mechanism without embellishment: “I don’t believe we shall ever have a good money again before we take the thing out of the hands of government.“

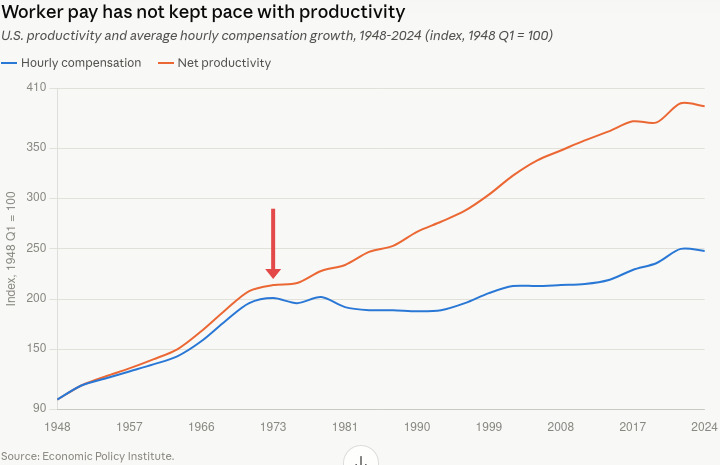

The chart tells a story that aggregate GDP figures are specifically designed to conceal. Real GDP per capita, real GDP per full-time worker, average real wages, and real median weekly earnings of full-time workers — five measures of the same economy — moved as a single bundle from 1947 through 1971. Then they didn’t. GDP per capita kept climbing at its prior trajectory, nearly quadrupling by 2014. Real median weekly earnings — the number closest to what an actual working American actually takes home — essentially stopped. Sixty-seven years of data, and the entire gain since 1971 accrued overwhelmingly to the top of the distribution while the median worker’s paycheck went nowhere. This is what “the economy grew” conceals when GDP is reported as a single number: growth continued, but stopped reaching the people producing it. Averaging hides exactly the divergence the average is built to obscure.

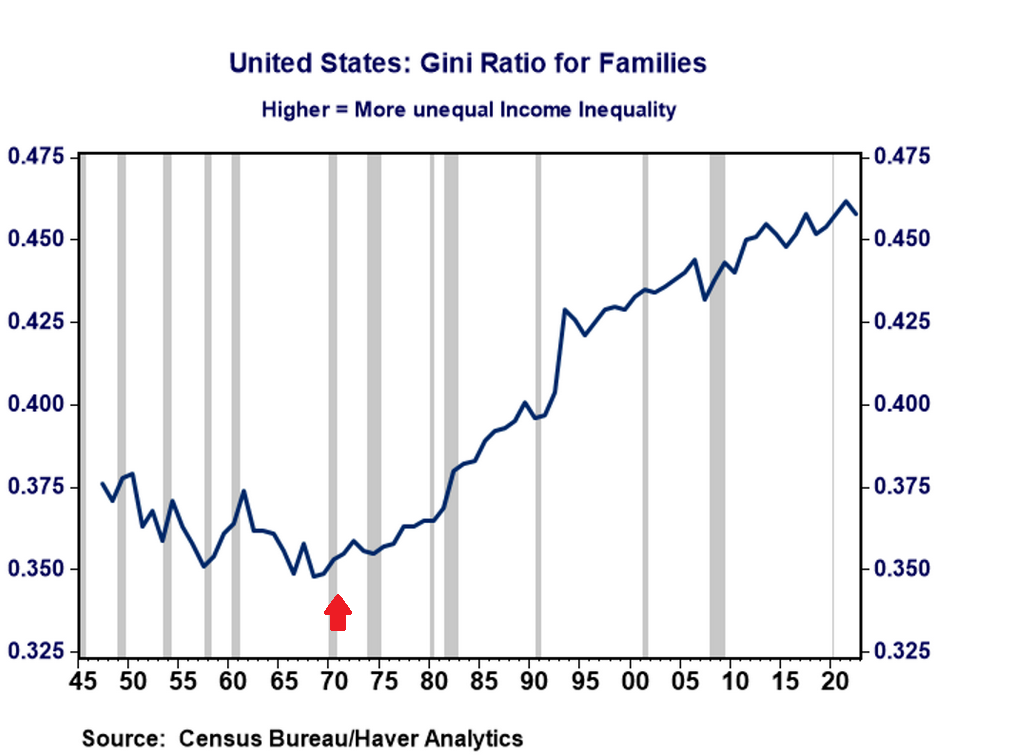

The Gini ratio for American families bottomed at 0.349 in 1971 — the lowest measured income inequality in the entire postwar series — and has climbed in nearly a straight line ever since, reaching 0.46 by the early 2020s, the highest ever recorded. This is not a story about the economy producing less. The GDP chart shows the opposite: aggregate output kept climbing. It is a story about where the output went. A family in 1971 could form a household on the median wage because the median wage still tracked the economy’s growth and inequality was at a fifty-year low. A family today is choosing whether to have children against a median wage that stopped tracking growth in 1971 and an inequality measure that has done nothing but rise since. The decision to have a child is, among other things, a financial decision. The financial conditions for making it changed permanently at the same moment everything else in this article changed – and fertility has been falling ever since.

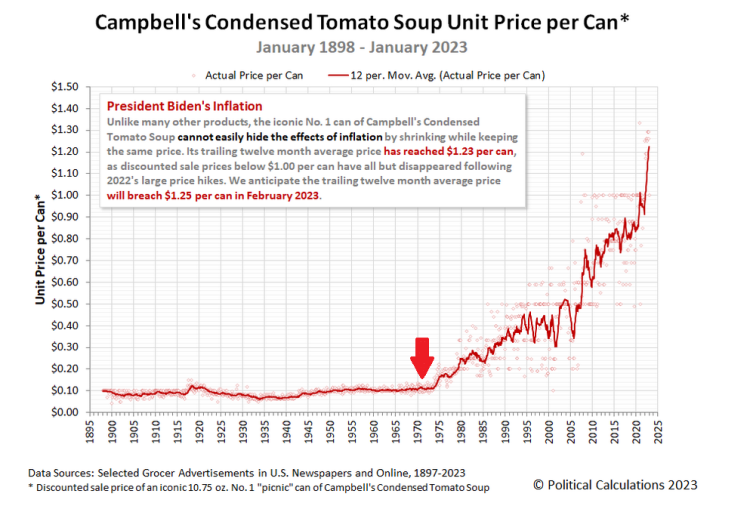

Campbell’s Condensed Tomato Soup has been sold in the same red and white can since 1898. The recipe hasn’t changed. The manufacturing process hasn’t changed. For 73 years the price didn’t change much either — a narrow, flat band from 1898 through 1971. Then it left the chart’s original scale entirely, climbing from roughly a dime to $1.23 by 2023, a twelvefold increase with no twelvefold increase in tomatoes, tin, or labor behind it. A can of soup is about as close to a pure measurement of currency debasement as the American economy produces. It has no brand premium to inflate, no technology story, no scarcity narrative. It is simply what happens to the price of something that hasn’t changed when the money measuring it has changed completely.

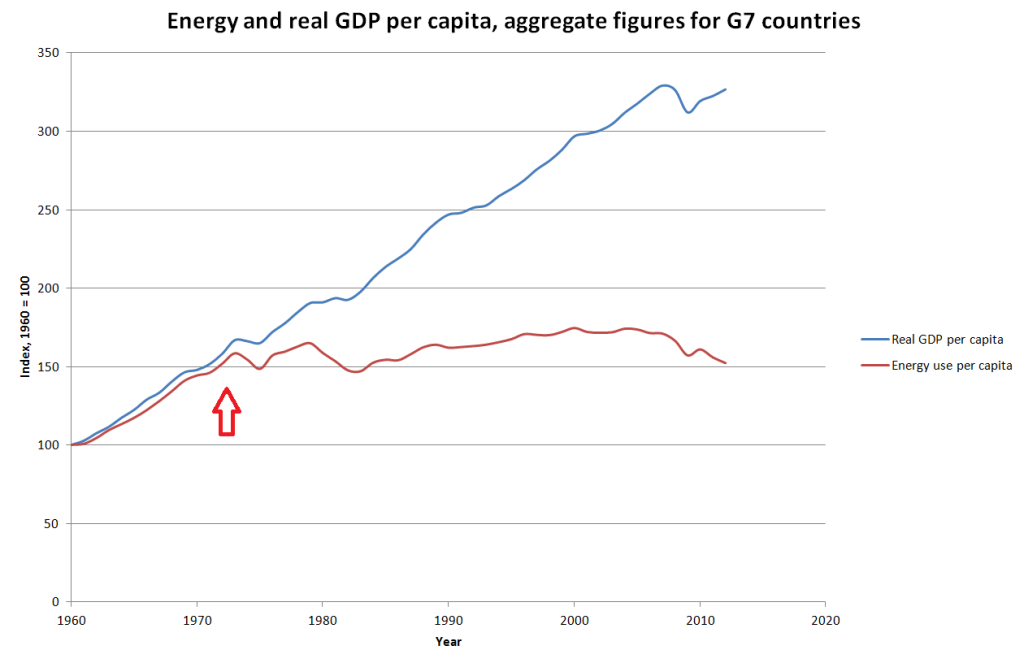

This is the same pattern, but it is no longer just an American story. Indexed to 100 in 1960, real GDP per capita and energy use per capita moved together across the G7 — the United States, Japan, Germany, France, the UK, Italy, and Canada combined — for more than a decade. Then, almost exactly in 1972-73, the two lines split. By 2012, aggregate GDP per capita across the world’s seven largest industrialized economies had more than tripled. Energy use per capita had grown by barely half that. Seven different central banks, seven different regulatory systems, seven different political cultures — and all seven economies decoupled output from physical energy throughput at the same moment. That is not a coincidence explainable by any single nation’s domestic policy. It is the signature of a global monetary system breaking simultaneously, because it was a global monetary system — Bretton Woods — that broke. Every currency in the G7 had been pegged, directly or indirectly, to the dollar’s gold convertibility. When Nixon closed the gold window on August 15, 1971, he did not just sever the American dollar from gold. He severed the entire postwar monetary order that the rest of the industrialized world’s currencies depended on. The chart shows what happened next, in seven countries, simultaneously: the relationship between paper wealth and physical wealth, broken everywhere at once.

Nixon called it temporary. The word did real work that Sunday evening — it transformed what was actually the permanent severing of the dollar from any external constraint into something that sounded like a brief technical pause, the kind of thing a sensible person didn’t need to worry much about. Most Americans watching that Sunday-evening broadcast reacted more or less the same way: well, OK, as long as it’s temporary. It was not temporary. Fifty-five years later, no administration of either party has ever proposed restoring the convertibility Nixon suspended that night. The word did exactly what it was chosen to do — it bought silence, and the silence became permanent.

VI. The 401K Pipeline

The elegance of the financialization architecture is that it eventually routes the productive economy’s own savings back through the extraction mechanism — and does so with the worker’s enthusiastic participation, because the tax incentive is genuine.

The 401(k) was presented as a democratization of investment: workers gaining access to the same asset appreciation that had previously benefited only the wealthy. The actual origin was less deliberate and more revealing. Section 401(k) was inserted into the Revenue Act of 1978 for an unrelated purpose — limiting executive profit-sharing plans — and sat unused for two years until a benefits consultant named Ted Benna found an aggressive reading of the provision that nobody had attempted before. His own client’s attorney refused to touch it, unwilling to be the test case for an interpretation that might draw IRS scrutiny. Benna implemented it on his own company instead. Within a few years, Congress recognized the scale of the tax revenue the loophole was costing the Treasury and tried twice to repeal it. Both attempts failed. By then, the interests that stood to profit from routing tens of millions of paychecks into perpetual, fee-bearing market participation — Wall Street, in the later and rueful words of the man credited with inventing the system — had organized enough to defend a structure nobody in government had designed and few in government still wanted. What survived was not an accident the system stumbled into and kept by inertia. It was an unintended discovery that served the right people well enough, quickly enough, that they made certain it could never be undone.

The tax deferral on contributions is real. The compounding benefit is real. The incentive to participate is rational. None of that changes what the structure was built to do once the worker’s money is inside it.

The 401K/IRA plans assume a life fewer workers actually get to live: steady employment to a chosen retirement date, decades of uninterrupted contributions, a market that cooperates with the calendar. For a worker who loses a job in their late fifties and can’t find another — not a hypothetical, but a routine feature of a hollowed-out economy that has spent fifty years thinning the mid-career job market for anyone over fifty — the 401(k) stops being a retirement plan and becomes the only asset left to live on. The withdrawal comes early, taxed as ordinary income at the exact moment income is lowest, often penalized, with none of the compounding the plan was sold on ever allowed to finish. The tax saving evaporates precisely when it’s needed most. That isn’t a flaw in an otherwise sound system. It’s what the system does to anyone whose life doesn’t match the assumption it was quietly built around. I know, because it happened to me.

What also happened: approximately $7-8 trillion in worker retirement savings flows overwhelmingly into mutual funds and index funds managed by Vanguard, Fidelity, and BlackRock. Most account holders assume this money sits, safe and static, the way it would in a vault — theirs, untouched, waiting. It does not. These firms collect management fees on assets they didn’t earn and didn’t risk, and the underlying securities are routinely rehypothecated: lent out through securities lending programs, posted as collateral for derivatives positions, and re-leveraged by the borrowing institutions in chains the account holder never sees and the monthly statement never discloses. The single share of an index fund sitting in someone’s 401(k) may, at the same moment, be doing triple duty as loan collateral two or three institutions removed from its nominal owner — earning fees for everyone in that chain except the person whose name is on the account.

By 2026 the pipeline has been extended one step further. AI infrastructure debt — bonds issued to finance the $700 billion annual hyperscaler buildout — is moving into retail retirement accounts through target-date and core bond funds. PIMCO anchored an $18 billion debt package for Meta’s Hyperion data center in Louisiana, booking $2 billion in paper gains at closing. PIMCO’s funds appear on major 401K platforms across the country. The PIMCO Income Fund alone manages $225 billion in assets drawn from American retirement accounts. Vanguard managed $1.79 trillion in target-date assets at the end of 2025. Approximately 61% of those assets are in passive strategies that track indexes mechanically — meaning the holder made no active decision to own AI infrastructure debt. The index bought it. The fund held it. The retirement account now carries it.

Larry Fink, CEO of BlackRock — the largest asset manager on earth, with $10 trillion under management — said explicitly that Americans’ pensions and savings accounts can fund the trillions required for AI data centers. He said the quiet part in a conference room full of people paid to hear it.

The loop is now visible in its entirety. The Fed creates fake money. It flows to the financial sector at the Cantillon front. The financial sector routes worker retirement contributions into 401Ks through tax incentives the workers rationally accept. The 401K money gets packaged into bond funds. The bond funds finance AI data center debt. The data centers are built with hardware dependent on Chinese-controlled supply chains the Pax Silica alliance cannot replicate. And the worker whose retirement savings funded the construction is the same worker whose job the AI is designed to eliminate.

No malice required at any individual point in the chain. Each participant optimizes for their return within the rules of the game as they find them. The rules were written by the people at the front of the Cantillon line, with money created by the institution those same people lobbied to preserve.

VII. The Forty-Year Invoice

“Merry Christmas, you wonderful old Building and Loan!”

— George Bailey

The 401K pipeline is not a new invention. It is the current iteration of a pattern that has been running since the New Deal — a pattern so consistent that it constitutes a law of government intervention in financial markets: artificial stability now, socialized losses later, larger intervention to paper over the previous one, repeat.

Frank Capra released It’s a Wonderful Life in 1946, and America took it as a celebration. The Bailey Brothers Building and Loan — taking local deposits, making local mortgages, run by people who knew their borrowers by name — was precisely the model the postwar regulatory architecture institutionalized. Regulation Q capped what banks could pay depositors, which capped what they needed to charge borrowers. The Federal Home Loan Bank system channeled government-backed cheap capital into savings and loan institutions whose sole purpose was residential mortgage lending. Federal deposit insurance, extended to S&Ls in 1934, backstopped the whole arrangement. My father got his 3% mortgage in 1963 because Washington had engineered exactly that outcome — and because the structural fragility underneath it wasn’t yet visible.

The fragility was there from the first transaction. S&L’s borrowed short — passbook savings accounts withdrawable on demand — and lent long — thirty-year fixed-rate mortgages. The arrangement works precisely as long as short-term rates stay below long-term mortgage rates. It is not a stable equilibrium. It is a deferred reckoning. When Paul Volcker raised rates to fight the inflation the Federal Reserve’s own money creation had produced, S&Ls found themselves paying depositors more than their mortgage portfolios were earning. By 1981 the interest rate spread had gone negative. A third of all S&Ls in the United States eventually failed. The federal bailout cost taxpayers approximately $130 billion. In a way, all the artificially low mortgages of the previous 4 decades were eventually paid by their children and grandchildren.

The official story treats Volcker’s rate hikes as the cure for an inflation that arrived from nowhere in particular — oil shocks, wage-price spirals, monetary mismanagement in the abstract. The inflation had an address. It began on August 15, 1971, the day the last external constraint on dollar creation was removed. Gold, the market’s own verdict on the currency’s credibility, went from $35 an ounce to over $800 within a decade. The Fed spent the late 1970s fighting a fire it had itself started nine years earlier — and the official accounts never once framed it that way, because doing so would have meant admitting the float itself was the mistake, not merely something that needed managing. Destroying a third of the nation’s S&L industry was, in that light, not an unfortunate side effect of necessary medicine. It was the bill finally arriving for a decision nobody in power was willing to reconsider.

Mr. Potter won. Just on a forty-year delay. George Bailey’s building and loan didn’t fail because it was badly run. It failed because the government policy that made it possible contained the mechanism of its own destruction — and when the bill came due, it was paid by taxpayers rather than by the architects of the policy. The gains, during the thirty years of artificial stability, were private. The losses, when the stability ended, were public. That distribution of outcomes was not accidental. It was structural.

This is the pattern. Not the S&L specifically — the S&L is merely the most cinematically perfect example. The same structure has run through every major financial intervention since:

Fannie Mae and Freddie Mac — government-sponsored enterprises created to subsidize mortgage liquidity, which became the primary transmission mechanism for the 2008 collapse. Bailed out at $187 billion in taxpayer cost. Now larger than before the crisis. The invoice was paid. The architecture was preserved. The next invoice is accumulating.

Student loans — federal guarantee removed credit discipline from educational lending, enabling tuition inflation that has outpaced general inflation for forty consecutive years. Total outstanding: $1.7 trillion. The S&L borrowed short and lent long against houses. The student loan program borrowed against the future productive years of eighteen-year-olds who couldn’t price the risk they were accepting. The houses at least existed. The degree’s labor market value was a projection.

Too Big To Fail — the 2008 bailout institutionalized the principle that systemically important financial institutions carry an implicit government guarantee regardless of how they got that way. The banks priced that guarantee into their risk models immediately and leveraged accordingly. In 2023, Silicon Valley Bank collapsed. Depositors above the formal $250K insurance limit — the limit that was supposed to impose market discipline on large depositors — were bailed out in full anyway. The moral hazard is now effectively unlimited regardless of the formal cap. The cap exists to maintain the appearance of discipline. The bailouts exist to ensure there is none.

The mechanism Rothbard identified in 1963 runs identically through every iteration: government intervention in credit markets creates the appearance of stability by suppressing the price signals that would otherwise discipline both borrowers and lenders. The suppression attracts participants who build structures on the assumption that the artificial stability is permanent. The structures become politically load-bearing — constituencies form around them, industries depend on them, elections get fought over them. When the suppressed reality eventually asserts itself, the losses are too large and too widespread to be allowed to fall on those who incurred them. The government intervenes again, at larger scale, creating the conditions for the next iteration.

The 401K is the current live example. Tax incentives route worker savings into financial markets, creating a constituency of asset-owning workers with a perceived interest in perpetuating the system. The retirement savings get packaged into bond funds holding AI infrastructure debt the workers didn’t choose and can’t exit independently. The AI being financed is designed to eliminate the jobs that fund the contributions. When the AI debt reprices — when the $700 billion annual hyperscaler capex that exceeds operating cash flow by enough to require continuous debt issuance encounters a refinancing environment that doesn’t cooperate — the losses will be inside the retirement accounts of people who had no framework for evaluating what they were holding and no ability to exit it independently of the fund.

The forty-year invoice for the postwar S&L architecture arrived in 1989. The invoice for the 2008 mortgage architecture has not yet been fully presented. The invoice for the AI debt now embedded in American retirement accounts is being written.

Each invoice is larger than the last. Each is paid by people further from the front of the Cantillon line than those who collected the gains.

VIII. The Lifecycle Extraction Sequence

The 401(k) is forty years old. The financial system has not been idle since. What has been constructed in the interim is a complete lifecycle extraction sequence — a set of mechanisms that intercept the worker’s financial resources at every stage of life, from before the first paycheck to after the last breath, leaving nothing for the generation that follows.

The sequence begins before the worker enters the workforce. Student loan debt now stands at $1.7 trillion across 45 million borrowers. A young worker begins their productive life carrying an average of $38,000 in debt at interest rates that compound faster than entry-level wages grow. Starting families, buying a first home, growing a nest egg, etc all have to wait until the loan is paid off. The financialization of education happened through the same mechanism as the financialization of retirement: a government program that transferred risk to the individual while transferring fee income to the financial sector.

The working years produce the 401(k) pipeline, but also a parallel extraction mechanism operating on the income leftover from the 401(k). Americans now spend $125 billion annually on lottery tickets — more than on music, movies, sports events, and books combined. It functions like a regressive tax: the adult living in the poorest 1% of zip codes spends nearly 5% of their income — $600 annually — on lottery tickets, while spending in the wealthiest zip codes is negligible as a percentage of income. The poorest Americans spend 33 times more of their income on lottery tickets than the richest. State lotteries pay out an average of only 60 cents of every dollar collected — and that figure flatters the actual return. The advertised jackpot is an annuity value spread over 20-30 years; winners who take the lump sum receive approximately half that figure before taxes, leaving a typical large-jackpot winner with roughly 30 cents of every advertised dollar after federal and state taxes. Those who accept the annuity receive annual installments funded by a contract the state purchases at wholesale from an insurance company, retaining the difference between ticket revenues and annuity cost. The lottery is not merely a bad bet. It is a financial product specifically engineered to appear more valuable than it is, sold overwhelmingly to the people least positioned to price the gap between the billboard and the check. The remaining 40 cents flows to the state, to the lottery administrators, and to the financial infrastructure that processes the transactions. The lottery is not a game. It is a voluntary tax on desperation, collecting from those with the least because the financial system has given them no other plausible path to the life they were promised.

The house is the last asset. For the American worker who managed to accumulate home equity despite everything documented above — the post-1971 wage stagnation, the student loan, the 401(k) fee extraction, the lottery — the reverse mortgage is the mechanism that converts the final accumulated asset back into a financial product. A homeowner who has spent thirty years paying down a mortgage trades the remaining equity for a monthly payment, surrendering the asset that would otherwise pass to the next generation. The nest egg, instead of being bequeathed to the hatchlings, is consumed by the system that spent forty years making it impossible to accumulate anything else. Seven out of ten Americans who reach 65 will eventually need long-term care — at a current median cost of $114,975 annually for a nursing home semi-private room, up nearly 50% since 2019. Those who die in hospitals average $32,379 in their final month alone; intensive care runs upward of $10,000 per day. One quarter of all traditional Medicare spending goes to beneficiaries in their last year of life. What the reverse mortgage didn’t extract, the end-of-life care industry does — at precisely the moment when cognitive and physical capacity to resist or negotiate is at its lowest. Private equity has systematically acquired nursing home chains since 2010, applying the same leveraged buyout model to elder care that it applied to retail chains and regional newspapers: extract fees, reduce staffing, hold the asset long enough to sell.

The newest mechanism doesn’t even offer the lottery’s 60-cent return. Stablecoins — dollar-pegged digital tokens backed by Treasury bills — now represent a $300 billion market processing $34 trillion in annual transactions. The business model is elegant in its simplicity: the private issuer collects your dollars, purchases Treasury bills with them, and collects the interest — approximately 4-5% annually. You receive a digital dollar that earns nothing. Tether earned over $10 billion in net profit in 2025 through this mechanism alone. The GENIUS Act, signed into law in July 2025, explicitly prohibits stablecoin issuers from passing yield to holders — legitimizing the extraction as permanent policy. It is the 401(k) fee mechanism with the pretense of investment removed entirely: there is no market exposure, no compounding, no promise of growth. There is only the spread, captured by the issuer, for as long as the holder remains in the system.

The full sequence assembled: student debt before the career begins, 401(k) fee extraction and lottery during the productive years, reverse mortgage against the house, end-of-life care against whatever remains, stablecoins monetizing the digital dollar itself. Each mechanism is presented as a service. Each is legal. Each was designed, lobbied into existence, and defended against reform by the same class of interests documented throughout this article — the Cantillon front-runners who receive the new money first and use it to build the next extraction layer before the previous one has been fully understood by its victims.

The nest egg does not reach the hatchlings. It is consumed en route, at every stage, by a system that has spent fifty years building exactly this architecture — and calling it financial services.

Every American baby born today enters the world owing approximately $133,000 in formally issued federal, state, and local government debt — before drawing a first breath, earning a first dollar, or making a single financial decision. That is the number politicians discuss when forced to discuss it. The Financial Report of the United States Government — the document the Treasury itself publishes — shows a more complete figure: when Social Security and Medicare’s 75-year funding shortfalls are included, the per-capita obligation rises to approximately $348,000. The House Budget Committee has cited $140 trillion in total unfunded liabilities on America’s balance sheet — approximately $419,000 per person. The Penn Wharton Budget Model’s infinite-horizon estimate exceeds $646,000 per person. The range depends on methodology. The direction does not. The generation that follows inherits every dollar of it, along with the depleted trust funds, the AI-financed infrastructure their parents’ retirement savings built, and the derivative tower erected on fifty years of wage stagnation. They did not make this world. They were born into it already leveraged — at any number between $133,000 and $646,000, depending on which promises you think will actually be kept.

When will that newborn pay off the debt? Per-capita formal debt is currently $133,000 and growing at approximately 6% annually. The median American worker’s lifetime federal tax contribution — every dollar they will ever pay in federal taxes across a 45-year career — totals roughly $554,000. At the current growth rate, the per-capita debt surpasses a 24-year-old’s remaining lifetime tax-paying capacity before they have paid a single meaningful year of taxes. By age 40 the per-capita debt exceeds $1.3 million. By retirement, $4.4 million. By death, if current trajectory holds, over $14 million — per person. This is not a debt that was meant to be paid off. Alexander Hamilton said so explicitly: a permanent national debt binding the bondholder class to the federal government’s perpetuation was a feature, not a defect. Two hundred and thirty-five years of compounding later, every American born today enters a lifetime of indentured servitude to an odious debt they did not incur, cannot vote to repudiate, and cannot individually escape — growing faster than they can earn, faster than the economy can grow, and administered by the same class of institutions that designed it to be permanent from the first day Hamilton put pen to paper.

Sooner or later, everyone sits down to a banquet of consequences.

— Robert Louis Stevenson, 1890.

X. Catherine Austin Fitts: the Financial Coup d’État.

Most analyses of financialization describe the mechanism without naming the intention. Catherine Austin Fitts names the intention. As Assistant Secretary of Housing, HUD, she oversaw billions in federal investment, until she raised concerns about systematic fraud and was subsequently subjected to a decade-long legal and regulatory assault documented in her Dillon Read & Co. analysis. She was eventually exonerated, and the Inspector General investigations documented billions in fraudulent losses.

She refers to a conversation she had in April 1997 with the president of CalPERS, “It’s too late. They’ve given up on the country, and they’re going to move all the money out of the country starting in the fall. They are moving it to Asia.” Many years later she came to realize “what he was talking about was they were implementing a financial coup. They had given up on a system where the bankers control monetary policy and the legislature, the people’s representatives, control fiscal policy and decided to move to a process where essentially the bankers controlled both fiscal and monetary policy, and they were not going to do it by you know presenting new legislation to change things. They were going to do it on the just-do-it method and lever up the debt, issue tons of debt and suck all the money out the back door and and essentially have a financial coup d’Etat, which is exactly what I think has happened.” She has spent thirty years documenting what she calls the Financial Coup d’État: the systematic transfer of public wealth to private control through a deliberate architecture of financial complexity, legal obscurity, and regulatory capture.

Her 2001 essay of that name — written from direct government experience — described the mechanism before most academic economists had named it:

“A financial coup d’état includes the removal of assets from the commons, the placing of the burden of outstanding liabilities on taxpayers, and the use of private and governmental power to control people through financial means.”

The conventional framing of 1990s capital flight describes a neutral market mechanism: American capital rationally seeking higher returns in lower-cost Asian manufacturing environments, comparative advantage functioning as designed. The CalPERS president’s statement describes something categorically different: a decision already made, by identifiable people, to move the capital out in the fall — three months before the Asian financial crisis that would retroactively justify the narrative of rational capital flight had even begun. The sequence matters. Decision first. Crisis second. Narrative third. The rational market explanation was constructed after the fact to describe a movement that had already been scheduled before the conditions used to explain it existed. This is not globalization as economics describes it. This is globalization as the CalPERS president described it in April 1997.

The missing $21 trillion — documented by Michigan State economist Mark Skidmore using the government’s own Inspector General reports, and subsequently obscured by FASAB Statement 56 — Fitts identifies not as accounting error but as the financial resources of the coup: money systematically moved outside the auditable economy before the audit mechanisms themselves were made legally optional. The government’s response — passing an accounting standard that made the obscurity legal rather than correcting it — just confirms that the movement was intentional.

What this article has documented across ten sections — the Hamilton feedback loop, the Cantillon front, the Fed’s reserve elimination, the 401K pipeline, the lifecycle extraction sequence, the per-capita debt trajectory that reaches mathematical inescapability within a working lifetime — Fitts frames as a deliberate architecture rather than an accumulation of policy errors. Each intervention she documented from inside HUD, each bailout that preserved the extraction mechanism at taxpayer expense, each regulatory change that transferred risk downward while protecting returns upward — these are not, in her analysis, the unintended consequences of well-meaning but misguided policy. They are deliberate policy designed by the people who benefit from it.

The endpoint of that architecture, as she describes it across years of interviews and research, is a transition from the current monetary system to a programmable CBDC control grid — in which economic participation becomes conditional on compliance with whatever the controlling institutions require, and the population that cannot generate sufficient surplus to justify inclusion is simply excluded from the economy rather than extracted from it. Not a dramatic event. A gradual withdrawal of the infrastructure the non-compliant depend on — the same infrastructure the series documents being built, layer by layer, from the Fusion Centers to the KIDS Act identity verification mandate to the stablecoin architecture that captures yield for issuers while passing nothing to holders.

The bail-in provisions of Dodd-Frank, the derivative seniority in the 2005 Bankruptcy Act, cooking the books that FASAB 56 legalized, the CBDC pilot programs currently underway — these are the components of a transition. Whether that transition is a grand scheme by coordinated actors or the emergent consequence of institutional interests Fitts answers only one way.

What is not open: the trajectory. The per-capita debt exceeds a 24-year-old’s remaining lifetime tax capacity before they have paid a meaningful year of taxes. The derivative tower exceeds the value of all global assets by an estimated $64 trillion. The music has been playing for fifty-five years. The chairs are fewer than anyone in authority will count publicly.

“We are at a crossroads,” Fitts has written. “We can choose to invest our money in a system that is trying to kill us, or we can choose to invest our money in a system that is trying to help us thrive.”

The choice she describes assumes there is still time to make it. The mathematics documented in this article suggests the crossroads is much closer than people expect.

But Catherine Austin Fitts has been warning that this coup will not stop with simply excludiing people from benefits. The endgame will be much more drastic. The successive government interventions, each one larger than the last, each one preserving the extraction mechanism at the cost of greater systemic fragility: Hamilton’s debt architecture, the Federal Reserve’s money creation, the 1971 gold window closure, the S&L bailout, the 2008 bailout, the 2020 reserve requirement elimination, the TARP bailouts, the CBDC transition now underway. Each intervention deferred the reckoning and made the next one larger.

I have repeatedly described official population control programs which have grown from mere family planning in 1965, to fertility control, to mass death. Catherine Austin Fitts said in an interview in Feb 2023, “The financial crew started bringing down life expectancy in what I call the great poisoning. So we’ve had a series of policies related to air, food, and water and to things happening through the FDA and pharmaceutical drugs [that] has really brought down the life expectancy because at that point the only way you could you could balance the books, if you weren’t going to do it financially, was to lower life expectancy and change the retirement benefits and that’s what’s been happening and has accelerated through the pandemic because we’re watching really a cratering of life expectancy in the United States.“

When a system’s liabilities exceed its assets by this margin, the “useless eaters” — pensioners, elderly, disabled and dependent — are the liability side of a ledger that cannot be balanced, the people who manage that ledger face a choice between default, inflation, and reducing the number of claims. Fitts names the third option. The documented trajectory names it too — the pattern of interventions has been building toward an endpoint that the mathematics makes inevitable and that the control architecture being constructed makes manageable for those who intend to be on the asset side of the final reckoning.

IX. What Was Lost

The system, diagrammed:

The real cost of financialization is not visible in any asset price. It is visible in what didn’t get built, what didn’t get made, what didn’t get started because the return on financial engineering exceeded the return on productive investment by a margin that made the choice obvious to anyone allocating capital.

The Midwest factory that didn’t open because the NEPA review would have taken seven years and the private equity return on a leveraged buyout was available this afternoon. The community bank that didn’t make the local business loan because the compliance cost of the new regulatory regime made small business lending uneconomical compared to mortgage securitization. The engineer who went to Wall Street to build derivative pricing models instead of physical infrastructure because the compensation differential was not marginal but categorical. The pension fund that stopped funding productive investment and started funding leveraged buyouts because the fee structure made the latter irresistible to the managers whose compensation depended on it.

These are not dramatic events. They don’t make the evening news. They are the accumulated daily decisions of rational actors responding to incentive structures that were systematically tilted against production and toward extraction — tilted deliberately, through policy choices made by people who benefited from the tilt.

Rothbard identified the mechanism in 1963: inflation is “a painless and all the more dangerous form of taxation” because it extracts without appearing to take. The financialization of the American economy is the same mechanism operating at civilizational scale: it extracted the productive capacity, exported the manufacturing base, converted the retirement savings into fuel for the next layer of speculation, and called each step of the process wealth creation.

The wealth was real. The creation was elsewhere.

“It is no crime to be ignorant of economics, which is, after all, a specialized discipline and one that most people consider to be a ‘dismal science.’ But it is totally irresponsible to have a loud and vociferous opinion on economic subjects while remaining in this state of ignorance.”

— Murray Rothbard

Read More

The Financial Coup

Catherine Austin Fitts, “Financial Coup d’État.” Solari Report, 2001. solari.com/financial-coup-detat/ — Fitts documents the Washington-Wall Street partnership that engineered a fraudulent housing bubble, illegally shifted capital out of the US, and used privatization as a mechanism to move government assets to private investors at below-market prices while shifting liabilities back to government. Written from direct experience as Assistant Secretary of Housing under Bush Sr.

Catherine Austin Fitts, “Financial Coup d’Etat“, Feb 2009. Fitts describes a global “heist” of capital being sucked out of country after country.

Catherine Austin Fitts, “The Financial Coup d’État: Missing Money for Beginners.” Solari Report / Corbett Report, 2019. solari.com/corbett-report-catherine-austin-fitts-explains-the-financial-coup-detat/ — covers FASAB 56, the missing trillions, and the back door in the US Treasury.

Catherine Austin Fitts interview on acTVismMunich , “The Financial Coup d’état Explained“, Feb 2023.

Catherine Austin Fitts interview with Andy Schectman, Miles Franklin Precious Metals, January 2026. marketsanity.com/catherine-austin-fitts-theyve-given-up-on-the-country-inside-the-financial-coup/ — Fitts explains why the global monetary system is no longer functioning as a currency system but as a control grid, with programmable money as the endpoint.

The S&L Crisis — Primary Sources Federal Reserve History, “Savings and Loan Crisis.” federalreservehistory.org

Lawrence J. White, “The Savings and Loan Debacle.” Econlib Encyclopedia of Economics and Liberty. econlib.org/library/Enc/SavingsandLoanCrisis.html — documents fifteen distinct government policies that caused the crisis.

Murray Rothbard, A History of Money and Banking in the United States. Mises Institute, 2002. Free PDF: mises.org — traces the Federal Home Loan Bank system and postwar mortgage subsidy architecture as direct extensions of New Deal interventions.

The Cantillon Effect — Primary Source Richard Cantillon, Essai sur la Nature du Commerce en Général, 1730 (published posthumously 1755). English translation: mises.org

Transmission Cost of Inflation

Jesús Huerta de Soto, Money, Bank Credit, and Economic Cycles. Mises Institute, 2006. mises.org — the most rigorous mathematical treatment of the round-by-round price transmission mechanism

Austrian School — Monetary Theory Murray Rothbard, What Has Government Done to Our Money? Mises Institute, 1963. Free PDF: cdn.mises.org/what-has-government-done-to-our-money.pdf

Ludwig von Mises, The Theory of Money and Credit, 1912. mises.org

Financialization — Academic Gerald Epstein, ed., Financialization and the World Economy. Edward Elgar Publishing, 2005.

Thomas Philippon, “Has the U.S. Finance Industry Become Less Efficient?” American Economic Review, Vol. 105, No. 4, 2015. Shows financial sector cost per dollar intermediated has not declined despite technology — the efficiency gains went to the sector, not the economy.

401K Pipeline into AI Debt “Your 401(k) Is Funding AI’s Data Center Buildout.” Seeking Alpha, May 14, 2026. seekingalpha.com/article/4904529

“AI data center debt might be in your 401k. Here’s how it got there.” Quartz, April 18, 2026. qz.com

“How AI debt ends up in your 401(k) target-date fund.” Quartz, May 8, 2026. qz.com

Larry Fink / BlackRock on pension funding of AI infrastructure: Moneywise, May 2026. moneywise.com

Reserve Requirements Eliminated Federal Reserve Board, “Reserve Requirements,” March 15, 2020. federalreserve.gov/monetarypolicy/reservereq.htm

Pax Silica “EU Joins US-Led Pax Silica Alliance To Secure AI Supply Chains.” Epoch Times / ZeroHedge, June 2026. zerohedge.com

Glass-Steagall Repeal Gramm-Leach-Bliley Act, Public Law 106-102, November 12, 1999. congress.gov

Manufacturing Decline Bureau of Economic Analysis, Value Added by Industry as a Percentage of GDP. bea.gov

Companion Articles “The Apotheosis of the Dollar” — the fake money system in full. “The Real Replacement” — the automation of the underlying productive asset. “The Digital Control Grid” — the programmable money replacement architecture.

Leave a Reply